By the end of 2024, the Belgian Parliament had transposed the EU Corporate Sustainability Reporting Directive (CSRD) into Belgian law. Consequently, the first entities legally required to report under this directive have recently released their inaugural reports. At this stage, amidst the complexity of the framework, key questions have emerged for executives, investors and other users of sustainability statements, including:

What patterns are emerging within the financial services industry?

How is the financial services industry adapting its disclosures given the absence of sectorial standards?

Which methodologies are entities employing to report on their financed emissions?

To provide some answers, we examined the CSRD statements from the Belgian financial services market, covering sectors such as banking, banking/insurance conglomerates and insurance. Our analysis focused on key metrics, ranging from the outcomes of double materiality assessments to the specific metrics outlined for topical disclosures.

This study provides a deeper understanding of the financial services sector in Belgium and offers comparative insights with the European market, based on the recent publication of PwC Global's analysis of 250 corporate sustainability statements across various industries.

Our analysis has revealed several trends and divergences in reporting practices, emphasising that entities are still adapting to the complexities of this new reporting regime and its application within the intricate landscape of the financial services industry. Are you interested in exploring this further and gaining additional insights into our research?

Read more about CSRD year 1

Key takeaways in the financial services industry & the way forward

What's in scope?

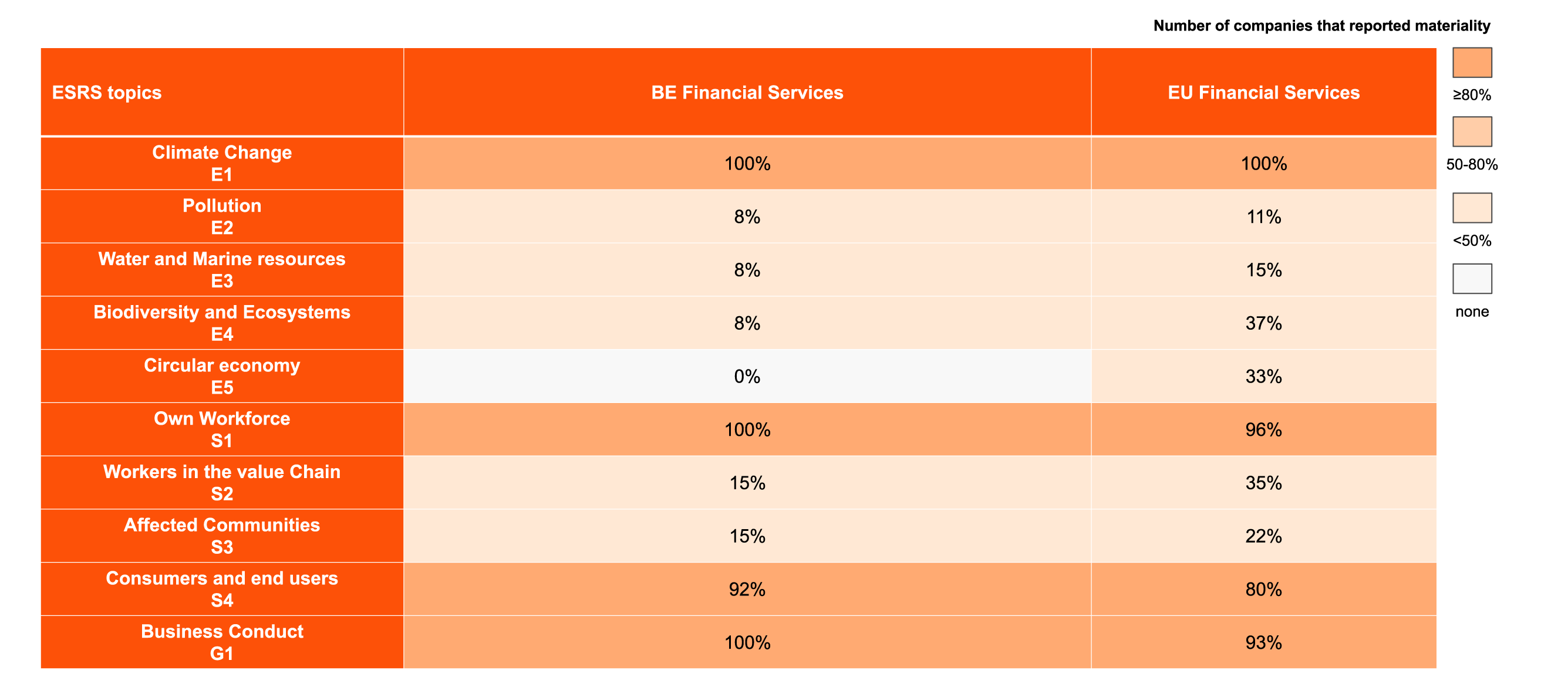

Under the ESRS, ten topical standards have to be considered by entities when performing their materiality assessment and reporting under the new regime.

In alignment with broader European trends, the most frequently reported topics for Belgian financial services are climate change, own workforce, consumers and end-users, and business conduct. This indicates that each analysed entity identifies and reports at least one impact, risk or opportunity associated with these topics.

However, one financial institution did not identify any material IROs associated with consumers and end-users due to their specific business model.

Conversely, a notable lack of consistency is observed in the Belgian market when considering other environmental and social topics. Unlike the European market, where specific environmental issues such as biodiversity are deemed material by a relatively high number of entities, this is not the case in Belgium.

Among the other environmental topics, circular economy is not reported on among the sample of benchmarked entities. Furthermore, the topics of pollution, water and marine resources, and biodiversity and ecosystems are infrequently deemed material.

Regarding other social topics, we noted that the topic of affected communities is occasionally reported on. In such instances, the topic is typically approached from a philanthropy perspective, highlighting the initiatives undertaken.

Emerging priorities: Sustainable finance, privacy and cybersecurity, innovation and other entity-specific topics

In addition to the disclosure requirements set by the ESRS, companies must provide additional entity-specific disclosures when they conclude that an impact, risk or opportunity is not sufficiently covered by one of the topical standards listed above.

In the Belgian market, almost all entities have introduced separate entity-specific topics. Those that did not explicitly include additional topics have aligned their entity-specific disclosures with existing ESRS topics. For example, one entity mapped data protection and privacy disclosures to the topic of consumer and end users.

In the reports that we have analysed, nearly half of the companies (46%) added an entity-specific topic regarding responsible investments/sustainable products and services. Considering the significance of the downstream value chain segment for financial services, we observe that entities are reporting on the sustainability considerations embedded in their products and services, frequently connecting these disclosures to the existing Sustainable Finance Disclosure Regulation (SFDR) framework.

It is worth noting that entities reporting on this topic often refer to a broad spectrum of environmental challenges within their disclosures, such as biodiversity, pollution and the water crisis, despite not deeming these topics material.

Privacy and cybersecurity emerge as another entity-specific topic of substantial importance, included by approximately one-third of the benchmarked entities (38%). This is linked to the scope and sensitivity of client data handled by financial services compared to other industries. Specifically, this topic is also increasingly relevant in the current context of digitalisation, with entities reporting on the positive societal impact, potential risks and opportunities arising from innovation of their products and the use of new technologies (31%).

Finally, around one-third of entities on the Belgian market include disclosures related to their financial resilience (31%), highlighting their societal role and linking these disclosures to their financial report.

This highlights the specificities that a financial services company deals with which are not encompassed by the generic topical ESRS standards.

Topics covered in CSRD sustainability statements: Comparison between BE and EU financial services

Entity-specific topics with highest occurrence for BE Financial Services (% of sample)

Navigating climate change disclosures

As previously mentioned, all entities benchmarked within the Belgian market have reported on the topic of climate change. More specifically, nearly all the analysed entities address the risks associated with climate change impacting their operations, which were usually identified following their climate risk scenario analysis.

Despite a consensus on the importance of the topic, disclosures regarding transition plans are often inconsistent. Among the entities analysed, fewer than half explicitly indicate having a defined and approved transition plan in place under the E1-1 disclosure requirement and compatible with the goal of limiting global warming to 1.5 °C. A common message across entities is that their transition plan is still under development.

Nevertheless, nearly all entities report on actions and targets for their emissions.

In terms of emissions, there is a wide consensus that Scope 3 emissions are most relevant for the financial services sector. Most benchmarked entities consequently report that Scope 3 categorical emissions are deemed significant beyond financed emissions.

Upon detailed examination, we find that most entities in Belgium have included disclosures regarding purchased goods and services, waste generated in operations, business travel, employee commuting and investments. These trends appear to be mirrored at the European level, where the same categories are emerging.

Beyond these common categories, the results are more scattered, making patterns difficult to identify. It appears that some entities, in addition to including emissions deemed material, have opted to report all available data or data that can be readily collected.

Across the BE and EU financial services, some categories of Scope 3 emissions were more common than others.

As indicated above, many entities are concentrating their climate disclosures on efforts taken to reduce Scope 3 emissions, which primarily includes GHG emissions associated with lending and investing (Scope 3 Category 15 - Financed emissions).

ESRS indicates that financial institutions shall consider the Partnership for Carbon Accounting Financial (PCAF), specifically Part A “Financed Emissions”. Although nearly all benchmarked entities reporting on financed emissions indicate reliance on PCAF methodology, the requirements related to reporting vary significantly.

In particular, regarding the minimum boundaries applied, not all entities disclose the percentage of coverage of their portfolio.

Additionally, concerning the type of emissions covered, there is growing concern among financial institutions about the lack of comparability and standardisation and the variability in reporting Scope 3 emissions of financed counterparties. Consequently, due to the estimation uncertainty, some entities decided not to report on this category.

A Focus on Diversity: Analysing Societal Impact Figures

As noted earlier, the own workforce topic is consistently reported within the Belgian financial services sector. Beyond the general disclosure requirements like employee characteristics under S1-6, there is a significant emphasis on diversity, equity and inclusion conforming to S1-9 and S1-16 disclosure requirements.

This focus aligns with recent European market trends prioritising diversity goals and initiatives. Indeed, almost all benchmarked entities indicate a link between variable remuneration and sustainability performance, with nearly half further reporting on diversity targets under the topic of own workforce.

Additionally, it also offers a novel perspective, as entities have not previously reported on harmonised metrics related to this topic.

In terms of results, we observe considerable variation in the figures reported in the statements we reviewed. The unadjusted gender pay gap averaged 16%, with values ranging from 1.9% to 31%. A common trend in the financial services industry is that most entities also disclose their adjusted gender pay gap*, which shows significantly lower figures. Similarly, the total remuneration ratio varies widely across the industry, ranging from 3 to 93, with an average of 23.

These results highlight considerable disparities among the benchmarked entities, suggesting a potential lack of common interpretation of the ESRS methodology and concepts.

* The adjusted gender pay gap enables entities to report on the gender pay gap in line with their own defined methodology (taking into account more elements than the ESRS defined calculation methodology).

Conclusion

As highlighted in the introduction, we are currently navigating the first wave of CSRD reporting.

Consequently, the insights provided in this article are general, reflecting the ongoing adaptation companies face with this new demanding reporting framework. While best practices are beginning to surface, the framework itself continues to be continuously challenged.

Within the context of the Omnibus package, two main components are tackled. First, the proposal would significantly reduce the number of organisations within the scope of CSRD and defer the timing of application for those entities that are in scope. Second, the package addresses the content of the directive itself, aiming to simplify reporting obligations by, for example, substantially reducing the number of mandatory data points to be disclosed. In addition, the proposals would remove a planned shift from ‘limited assurance’ to ‘reasonable assurance’.

It is important to keep in mind that the package currently remains at a proposal stage and that it may still be subject to important changes in the coming months, with the potential changes undergoing a fast-track legislative process.

Despite the evolving framework, the journey is underway and there is no turning back. Embrace the opportunities ahead and leverage our insights to confidently navigate future evolutions.

About the authors