The minimum ETR of 15% in practice

Pillar Two aims to ensure MNEs pay a minimum ETR of 15% across all their jurisdictions. This means that earnings in countries where the MNE’s ETR is less than 15% (as determined by the Pillar Two rules) will be subject to an additional top-up tax. This also includes operations that occur in jurisdictions that either do not implement or have been delayed in implementing the rules.

It is worth noting that countries that enact Pillar Two may be able to impose additional tax on foreign-headquartered MNEs if the tax imposed by the foreign jurisdiction on the profits in such jurisdiction of these MNEs is less than 15%. In some cases, although the foreign nominal corporate income tax rate might be above 15%, certain credits (including the R&D tax credit), deductions and incentives could cause the effective tax rate on these foreign operations to fall below 15%.

How MNE tax is assessed

The Pillar Two rules include three mechanisms for assessing tax on a MNE’s income, and MNEs will have to comply with the filing requirements for each applicable rule:

- The (qualified) domestic minimum top-up tax ((Q)DMTT) is imposed on income earned within a country’s borders to ensure that the income is taxed at a rate of 15% for Pillar Two purposes.

- ·The so-called primary rule is the income inclusion rule (IIR), which generally imposes tax on the parent entity of an MNE group to the extent that the foreign subsidiaries of the MNE are taxed at a rate less than 15% as determined for Pillar Two purposes.

- The IIR is accompanied by a backstop rule, also known as the undertaxed profits rule (UTPR), which permits a country to impose additional tax on an entity if that entity has any affiliated entities in other jurisdictions that are taxed at less than the 15% Pillar Two rate.

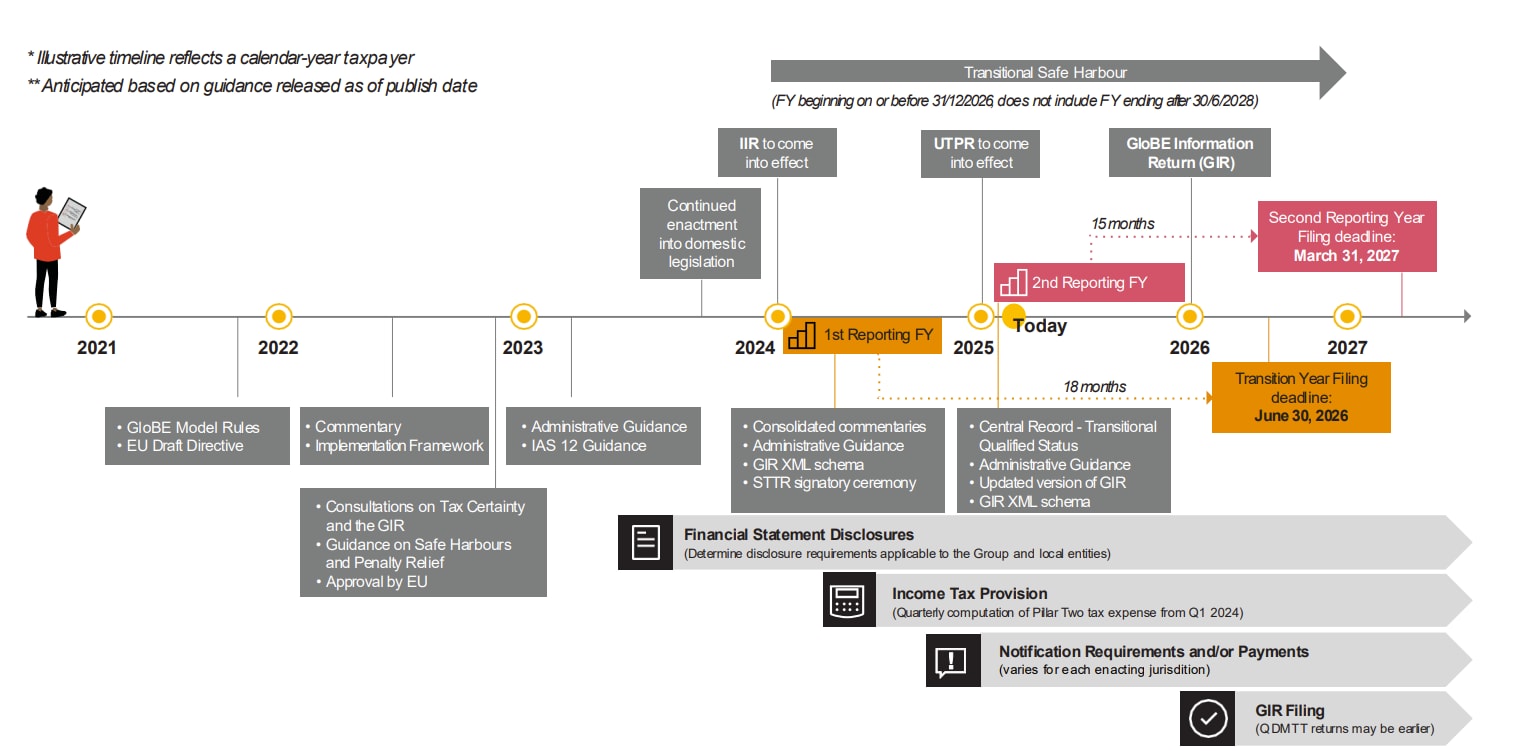

Pillar Two timeline

The Pillar Two rules are effective starting for fiscal years beginning on or after 31 December 2023 (for (Q)DMTT and IIR) for EU Member States and certain third-country jurisdictions. Compliance with new annual tax filings will start as early as 2025, but will generally be due in 2026, with some jurisdictions imposing notification requirements and/or estimated payments that started in 2024 or 2025.

This strict timeline means MNEs should already be developing the framework for data, technology and processes for global and statutory compliance.

The first step looks at operational changes. From stakeholder management and governance to response planning and budgeting, every aspect of the MNE’s operations should be assessed in light of Pillar Two’s requirements.

This step determines which financial consolidation groups are subject to Pillar Two rules before evaluating the GAAP and/or IFRS financial statement preparation process. Understanding this is critical for the MNE to start to implement Pillar Two.

Step three focuses on safe harbours. This starts by evaluating current country by country reporting (CbCR) processes, data and output, before analysing which jurisdictions could qualify for safe harbour and the benefits of opting in.

This step evaluates your current data and system structures to identify and remediate data and system gaps. This enables MNEs to develop and implement data strategies rooted in systems and processes.

Step five looks at the financial statement reporting requirements. This includes understanding Pillar Two disclosures and determining income tax provision impacts. MNEs should also review the technical nuances of the Pillar Two rules to understand how these changes are likely to impact their organisation.

The last step is about the Pillar Two compliance obligations. While these are strict, Pillar Two’s extended timeline provides some additional time to consider and prepare.

Is your EMEA multinational enterprise ready for Pillar Two implementation?

Download our Pillar Two Guide (EMEA) - March 2025 edition